Renting vs. Buying: The Numbers Might Surprise You

Why Many Renters Are Re-Thinking Their Next Move

Renting can often feel like the easier choice. There’s less responsibility for maintenance, fewer upfront costs, and the flexibility to move when needed. But when you look closely at the numbers, the long-term financial impact of renting versus buying can be surprising.

Recent housing market data shows that in many parts of the country, buying a home can actually be more affordable than renting when you compare monthly costs. This shift is being driven by moderating home price growth, more housing inventory, and improving mortgage rate conditions.

For many renters who believe homeownership is out of reach, the math may tell a different story.

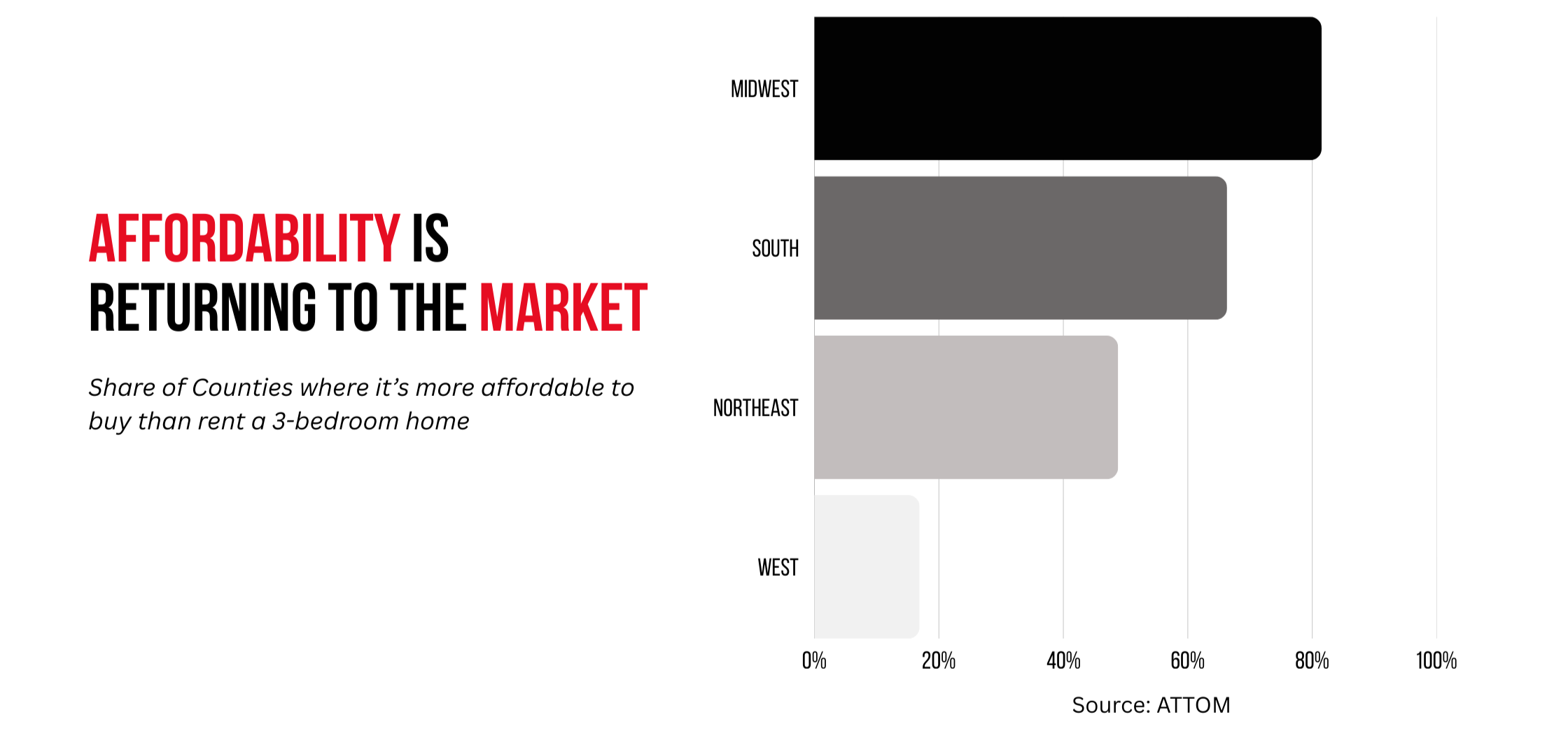

Buying Is Now More Affordable Than Renting in Many Areas

According to recent housing data analyzed by economists, buying a home is more affordable than renting in 57.7% of U.S. counties.

Several factors are helping make this possible:

• Slower home price growth compared to previous years

• Mortgage rates easing from recent highs

• More homes available on the market

• Rent prices remaining elevated in many cities

While affordability varies depending on the local market, the trend is clear: in many places, renters may actually spend as much or more per month than homeowners.

Renting Builds Someone Else’s Wealth

One of the biggest differences between renting and owning comes down to equity.

When you rent, your monthly payment goes directly to your landlord. At the end of the lease, you do not retain any financial benefit from those payments.

When you own a home, however, a portion of every mortgage payment contributes to building equity in a property you own. Over time, that equity becomes part of your net worth and can create financial opportunities later in life.

For many homeowners, their house becomes their largest long-term asset.

Homeownership Can Provide Long-Term Financial Stability

Another major advantage of owning is payment stability.

With a fixed-rate mortgage:

• Your principal and interest payments stay consistent

• Housing costs become more predictable

• You are less exposed to rising rent prices

Renters, on the other hand, often face rent increases when leases renew, making long-term budgeting more difficult.

The Biggest Misconception Holding Renters Back

One of the most common reasons people continue renting is the belief that buying requires a massive down payment.

In reality, many buyers qualify for loan programs that require far less upfront cash than most people expect. First-time buyer programs, grants, and low-down-payment loans are widely available.

For many renters, the biggest barrier is not financial qualification, but simply not knowing what options exist.

Curious What Buying Could Look Like for You?

Renting can feel like the simpler option, but the numbers show that buying may be more attainable than many renters realize. With improving affordability conditions and more homes available, this could be a good time to explore what homeownership might look like.

A quick conversation can help answer questions like:

• How much home could you realistically afford

• What your monthly payment might look like

• Whether buying now or waiting makes more sense for you

You might discover that homeownership is closer than you think.

Stay Connected

Ranked among the top 1% of real estate teams in the Chicagoland market, Cory Tanzer and the Cory Tanzer Group are experts in helping buyers and sellers navigate today’s market across Downtown Chicago, the North Shore, and the Western Suburbs. Recognized for their neighborhood expertise in areas like University Village, University Commons, South Loop, and Pilsen, the team helps clients stay one step ahead by understanding where the Chicago market is moving next.